Compound interest, e, and

i/Chapter 11

The important thing about doing most math is that we

really want more than the answer, we want to generalize the answer, to find the

answer for any problem like we're workin on.

Ian, at age 11, came to Don with the problem- what would his Dad pay in monthly

installments on a house worth $10,000 at a 10% annual interest, with a 30 year

mortage? He really wanted a number for an answer. This got us working on the

simpler problem of investing and finding the interest.

I must say that I don't know everything, and make a lot

of mistakes, in spite of what my students might believe. So I wasn't able

to give Ian a quick answer, but he and I worked very hard to solve his problem.

We started this way, and came to a place where most people can do this- patterns

are so important and make things simple. Just last evening I asked Will what

compound interest was. He is in an advanced algebra class doing this. He gave me

a formula, but didn't really understand what it meant. I went through the

following discussion with him (he was trying to fight it most of the way, but

finally saw the light!)

1. Simple interest. Find the amount you

have in the bank after 2 years if you put in $1, at a 6% annual rate of

interest. (It will always be an annual rate of interest with all the problems

below.)

The Interest = Principal * rate * time

The Interest (for

2 yr) = $1 * .06 * 2 = $.12 and the

amount (A) you would have after 2 years

A = P + I = $1 + $.12 = $1.12 Notice that the interest is not added each year

to get a new principal.

2. Compound interest- leading to a very important infinite

sequence. Here

the interest is added after each compounding period.

The Interest = Principal

*

rate * time = P*r*t and the Amount = P

+ I

Find the amount you have in the

bank after 1 year, with a principal of $1, at 6% annual rate of interest,

compounded semi-annually or 2 times per

year.

The interest earned during the first (1/2)

year = I(first 1/2 year) =

$1*.06*(1/2) = .06/2

($.03)

Now find the Amount you have in the bank

after the first (1/2) year

Amount = P

+ I = 1 + .06/2

= $1.03 which will also be the new principal for the 2nd 1/2 year. [If you don't

do the arithmetic, and leave out the dollar sign, you will find the pattern quickly].

Interest (2nd 1/2 year) = (1

+ .06/2)* .06/2

Amount (after 2-(1/2)years)= P

+ I =

(1 + .06/2)

+ (1 + .06/2)*.06/2

Factoring out (1 + .06/2)

from each term above, we get (1 + .06/2)(1 + .06/2),

The algebra looks a little tricky, but is just the

distributive property. a is the common factor.

We have a + a*b = a*(1+b) because the right side is

a*1+ a*b = a + a*b. In the case above

a= (1 + .06/2) and

b= .06/2. So if we

factor

(1 + .06/2)*1

+ (1 + .06/2)*.06/2 = (1 +

.06/2)(1 +

.06/2)

So the Amount (after 2

-(1/2)years, or 1 year) = (1 + .06/2)(1 + .06/2)

= (1 + .06/2)2

= 1.124 (more than the simple interest after 2 years).

What would the amount you have in the bank after

1 year, putting in $1, at 6%,

compounded quarterly (4 times per year)? Can you predict what this will

be? Let's look at it.

The interest earned during the first (1/4)

year = Interest(first 1/4 year) = P*r*t =1*.06*(1/4) = .06/4

(Notice: the r*t = .06*(1/4) = .06/4)

Now find the Amount you have in the bank

after the first (1/4) year

Amount (after the 1st (1/4))= P

+ I = 1 + .06/4,

which will be the new principal for the 2nd 1/4 year.

Interest(2nd 1/4 year) = (1

+ .06/4)* .06/4

Amount(after 2-(1/4)years)= P

+ I =

(1 + .06/4)

+ (1 + .06/4)*.06/4

Factoring out the term

(1 + .06/4), we get (1 +

.06/4)(1 + .06/4), so

the

Amount (after 2

-(1/4)years, or 1/2 year) = (1 + .06/4)2

Interest(3rd 1/4 year) = (1 +

.06/4)2

*.06/4

Amount(after 3-(1/4)years)= P

+ I =

(1 + .06/4)2

+ (1 + .06/4)2

*.06/4

Factoring out the term (1 + .06/4)2

, we get (1 +

.06/4)2(1 +

.06/4), so

the

Amount (after 3 -(1/4)years) = (1 +

.06/4)3 See

the pattern?

What would the amount you have in the bank after 1 year, putting in $1, at

6%, compounded quarterly (4 times per year)?

(1 + .06/4)4

= 1.061363551

What would the amount you have in the bank after 1 year, putting in $1, at 6%,

compounded monthly (12 times per year)? (1

+ .06/12)12

= 1.061677812

What would the amount you have in the bank after 1 year, putting in $1, at 6%,

compounded daily (365 times per year)? (1

+ .06/365)365

= 1.061831311

What would the amount you have in the bank after 1 year, putting in $1, at 6%,

compounded 10,0000 times per year? (1

+ .06/10,000)10,000

= 1.061836355

What would the amount you have in the bank after 1 year, putting in $1, at 6%,

compounded continuously, (an infinite number of times per year)?

We end up with an infinite sequence

1.124, 1.061363551, 1.061677812, 1.061831311, 1.061836355,

... which converges to

limitn->inf(1

+ .06/n)n

= 1.0618363547... and equals the very important number e.06

!!

So e1 = e = limitn->inf(1

+ 1/n)n

What would be the amount you have in the bank after

2

years, putting in $1, at 6%,

compounded monthly (12 times per year)? (1

+ .06/12)12*2

= $1.127159776

What would be the amount you have in the bank after

2 years, putting in $500, at 6%,

compounded monthly (12 times per year)? 500(1

+ .06/12)12*2

= $563.5798881

What would be the amount (A) you have in the bank after t

years, putting in P dollars, at

an annual rate of interest r,

compounded n times per year)?

A = P*(1+

r/n)n*t

What would be the amount (A) you have in the bank after t

years, putting in P dollars, at

an annual rate of interest r,

compounded continuously? We need

limitn->inf(1

+ 1/n)n to get

e.

We'll do a little algebra, starting with A = P*(1+

r/n)n*t

,

using the fact that

r/n

= 1/(n/r)

then A = P*(1+

r/n)n*t

= P*(1+

1/(n/r))n*t.

Now let m =n/r, and

substitute m in place of n/r,

we get

A = P*(1+

r/n)n*t

= P*(1+

1/(n/r))n*t

= A = P*[(1+

1/m)]n*t

.

Since n=m*r,

we can substitute (m*r)

for n

in the exponent A = P*[(1+

1/m)]n*t

obtaining

A=P*[(1+

1/m)]m*r*t

. Now using the identity for raising a

power to a power, this can be written as A =P*[(1+

1/m)m]r*t

, then

compounded continuously,

A =P*[limitm->inf(1+

1/m)m]r*t

The amount (A) you have in the bank after t

years, putting in P dollars, at

an annual rate of interest r,

compounded continuously, is

A=P*er*t

See Katie's work on compound

interest #3

Kirsten works on

(1+.07/x)x

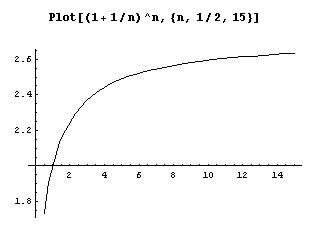

On Sept. 10, 1996

Kirsten, at age 15, (she had started with Don at age 5) was working on this

problem (using .07 instead of .06) for her calculus class. We graphed (1

+ .07/x)x in Derive,

but couldn't import it into a paint program and then to a gif file. So we

graphed it in Mathematica and

got this:

Here are some of the things we explored in Mathematica and Derive with

some surprising and exciting results:

(1 + .07/-0.1)-0.1 =

1.12794, a real number. Check the graph.

(1 + .07/0)0 =

1 This was hard to believe, but the graph bears it out!

(1 + .07/0.001)0.001 =

1.00427

(1 + .07/-0.07)-0.07 Mathematica gives:

"Power::infy: Infinite expression 0.-0.07 encountered.

ComplexInfinity." as the answer. Derive gives

" + or - infinity" as the answer.

(1 + .07/-0.01)-0.01 =

0.981757 - 0.030853i ;

which makes sense when you look at the graph.

limitx->0(1

+ .07/x)x =

1

limitx->0,Direction->-0(1

+ .07/x)x Mathematica gives:

"Power::infy: Infinite expression 1/0 encountered. Infinity::indet:

Indeterminate expression ComplexInfinity" 0encountered.

Indeterminate"

limitx->infinity(1

+ .07/x)x =

1.072508181254216 and e.07 =

1.072508181254216

The graph of (1 + 1/n)n by Geoffrey

in Mathematica' . ( also see chapter

11)

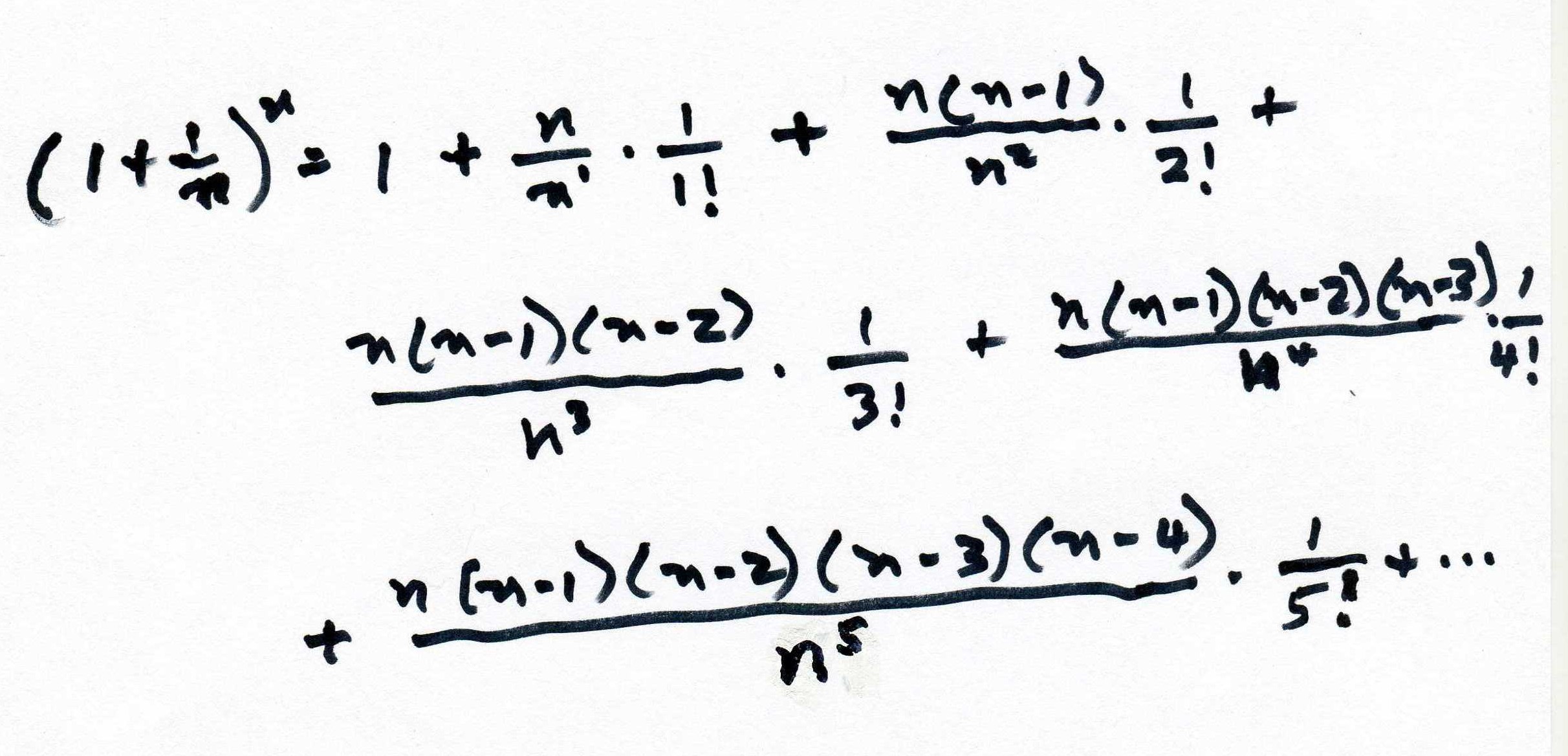

Naming e and ex as an infinite series

Using the binomial expansion from chapter 9, the first 6 terms of (A + B)n

are:

Substituting 1-> A and 1/n-> B

We'll simplify this: in the terms with 1 to any power, that's 1, and the

powers of n are exchanged with the factorials since they are multiplied, to get:

We've gone out 6 terms of the binomial expansion, now we'll look

at what happens when we let n -> infinity. All the fractions with n's will go

to 1 (subtracting 1 and 2, etc. in the top as n gets very large, won't affect

that), and we get:

The above gave us e1.

Can you find the infinte series for ex

using the binomial expansion? Just substitute the

same1->A, and x/n ->B and see what you get. We'll come

back to this in a bit.

Patterns with i

In the history of mathematics,

someone came along with the equation 3 + x = 1, and people said "Oh, you

can't do that". Someone else invented the integers and was able to solve

the equation putting -2 in for x to make the sentence true. Sometime

later, someone came up with the equation x2

= x.x = -1 and remember rule for substitution, in

one open sentence you have to put the same number in for each x. If you try 1x1= 1, and -1 x -1= 1,

neither of these work. Some kids try -1/2 x -1/2, but that

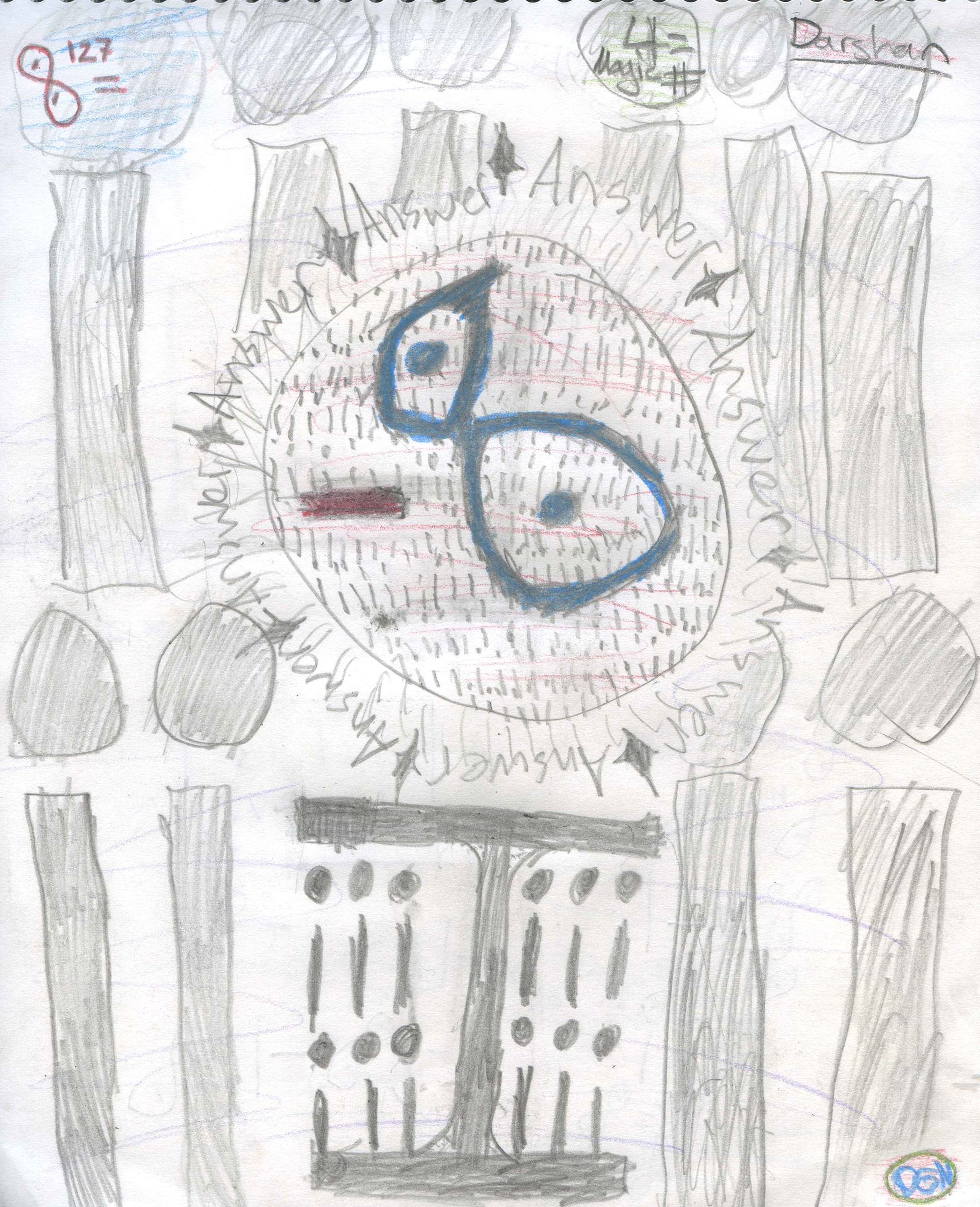

is 1/4, not -1. Darshan, a 4th grader, said the answer was unreal,

and invented the symbol below- looks like tilted "i glasses"- to solve the

problem and proceeded to find powers of i. Don encourages students to

make up other symbols, because the symbols are not the important thing, but what

it stands for.

Darshan found a pattern in the powers of i,

just above. i0=1,

i1 =i,

i2 =-1,

i3 =-i,

then this pattern continues in groups of 4. Don left Darshan with the problem of finding i127.

He found it to be -i,

which he drew below with a lot of flair!! Notice also that 4 = magic #,

which he found as the pattern above.

Fine work, Darshan!

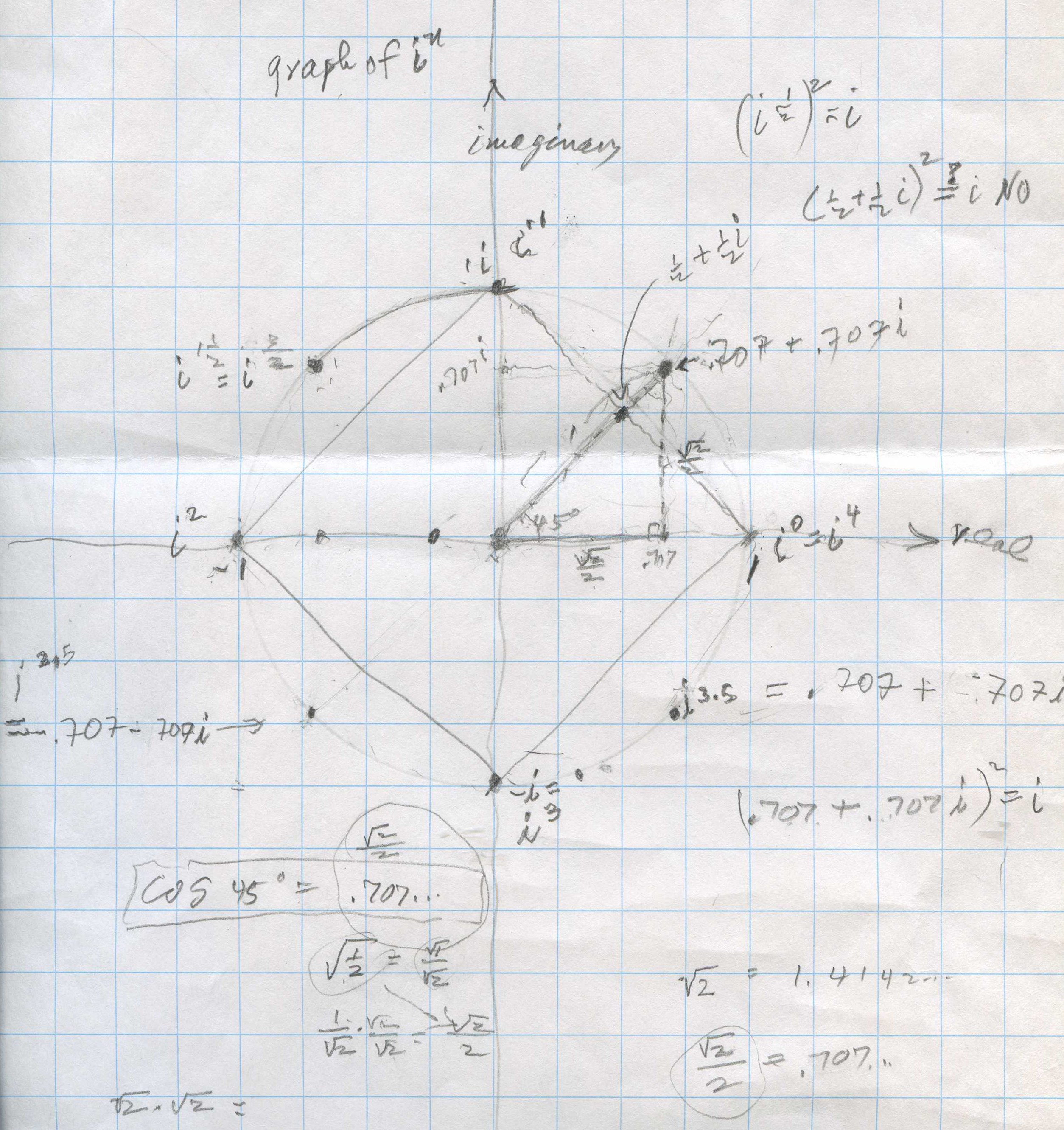

Shaleen, a 6th grader,

graphs in, finds

i1/2, and

finds the graph is not a square!

Don asked Shaleen to graph in

for n = whole numbers.

[Note: the vertical axis is the imaginary axis with the scale 4 units = 1i,

and the horizontal axis is the real axis, with the scale 4 units = 1]. He knew

that i0=1,

i1 =i,

i2 =-1,

i3 =-i

and i4 =1,

so he plotted those points below. Most youngsters believe right away that these

points are the corners of a square, which he drew. When Don asked Shaleen where

i1/2

would be, he put a point half-way between i0=1

and i1 =i

on the square. This point is represented by the complex number

1/2 + (1/2)i

and he thought would be i1/2

. Don said that if i1/2

is squared, that would = (i1/2)2

which

= i because raising a power to a

power, you multiply the exponents (which he knew). So Don had Shaleen square 1/2

+ (1/2)i below.

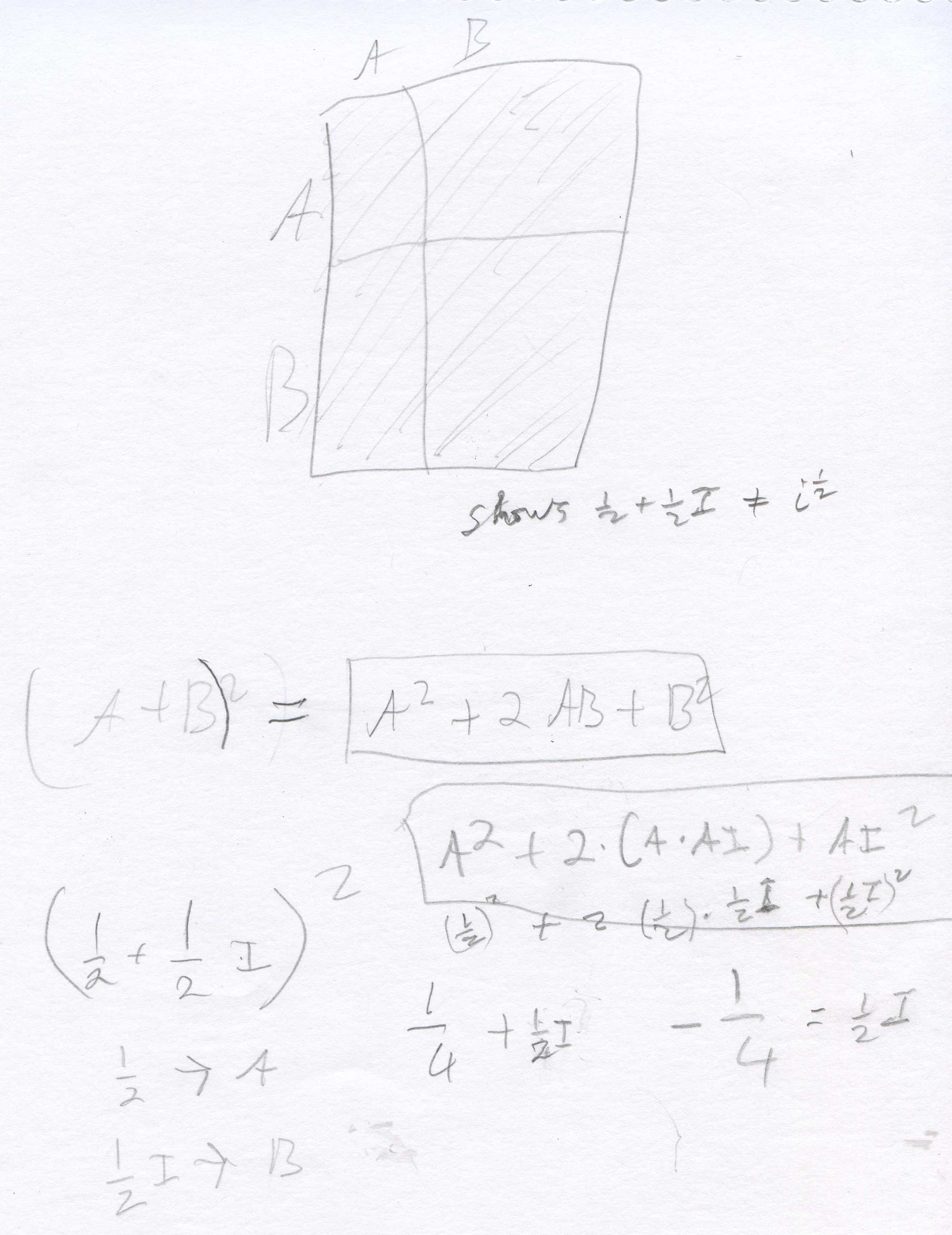

Don uses the area model for (A+B)2

= (A+B)(A+B), and Shaleen substituted 1/2->A and 1/2 i ->B. He

found that [1/2 + (1/2)i]2

= 1/2 i, NOT i. So 1/2

+ (1/2)i is not = i1/2

!

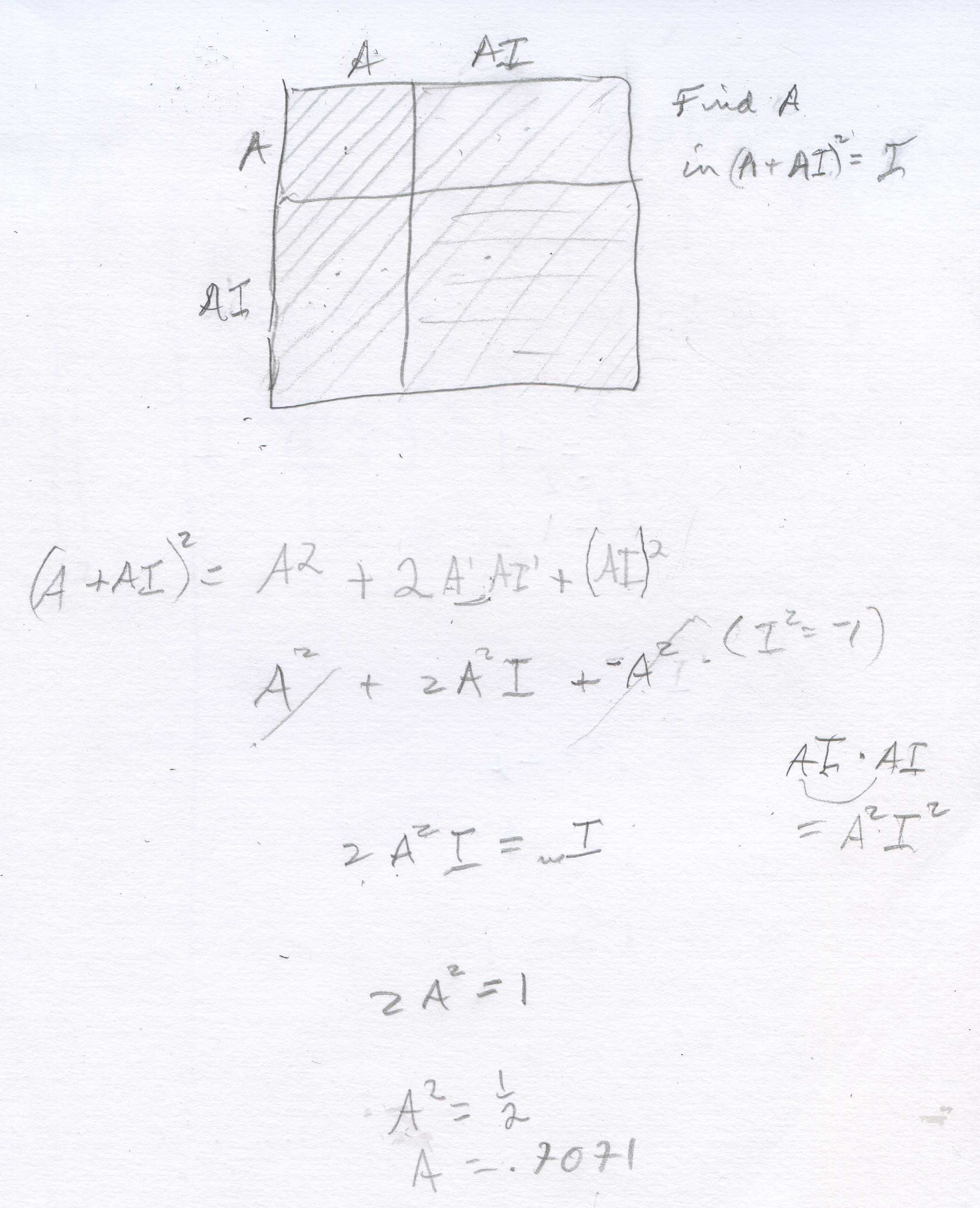

At this point Don suggested a way Shaleen

could find i1/2

. Since the point is half-way between i0=1

and i1 =i,

we can use the point (A + Ai) to keep it on the y=x line, square it and set that

number equal to i to find A. Shaleen proceeded to do this below.

Note, if 2A2i =

something times i, the something must = 1, so 2A2 = 1.

He got A= the square root of (1/2) = .707... So i1/2

= .707..+ .707...i, which Shaleen was able to plot on the first graph, repeated

below. Don had Shaleen use the calulator to find the sqrt(2) then divide by 2

and he got .707... THAT NUMBER AGAIN! They talked about if he knows that point,

what other points can he plot? He plotted points at i1.5,

i2.5

= -.707..-

.707..i , and

i3.5

= .707..- .707..i .

At one point Shaleen put in

the calculator -.707..-

.707..i, hit ENTER, and got -1-

i which he knew was wrong. What happened? It turned out that the calculator was

set for 0 decimal places, and had rounded off the numbers to 1. What is (.707..+

.707..i)2 ?

Shaleen got out the compasses and constructed a circle of radius 1 that went

through these points. Don drew a right triangle in the first quadrant, mentiond

that the length of the hypotenuse was 1, the radius of the circle, then asked

Shaleen the measure of the other 2 angles, besides the right angle. They turned

out to be 45' each because the sides are both equal to .707..Then he asked him

to find the length of the 2 sides that form the right angle. At first he said 1,

because 12

+ 12

= 12 but quickly

realized that couldn't be and said x2

+ x2

= 12 and 2x2

= 1, so x = sqrt (1/2) = .707... Don had Shaleen look up

on his calculator the cosine of 45'

which is .707.. We had to stop, and will continue the trigonometry we had

started earlier.

Fine work Shaleen!

Graph

of iterating in,

starting with n = i

Before Mathematica I

never would have seen this graph! Notice, another spiral! (Actually there are 4

spirals here if you look at the endpoints of the segments). And ii is

a real number! (Can you prove that?) Amazing stuff here. One

of the finest math sites on the internet, which has interactive applets, is IES

in Japan. One applet they

made was inspired by the graph above, is under complex

number i^(i^i..). You

can drag the point at 0+1

i

around

the complex plane to get some amazing things!! (You need to download Java (free)

to see these).

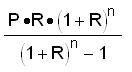

Back to Ian's problem,,,what would his Dad's monthly payment on

a $10,000 house loan at 10% for a 30 year mortgage be? We did it with a lot of

work- M is the monthly payment, n is the number of payments (12x30=360), R is

the monthly rate of interest= .10/12, P= $10,000

Generalizing

for n payments, we get

M =  and

our problem is solved,

and

our problem is solved,

M

came

out

to be about $87+/month.

See

Chapter 11 Questions and answers.